Custom mobile wallet solutions are the infrastructure backbone of modern digital financial services. But with dozens of mobile wallet solution providers crowding the market, how do you separate a platform built for the long haul from one dressed up to win a demo?

Industry specialists like 6D Technologies have spent years engineering what a truly enterprise-grade custom mobile wallet solution looks like, and the gap between their standard and the average vendor’s offering is wider than most buyers realize before it’s too late.

In this blog, we break down the non-negotiable features that every custom mobile wallet solution must have before it earns a place on your shortlist. We’ll cover security architecture, open API interoperability, regulatory compliance configurability, real-time scalability, merchant and agent network tooling, loyalty and value-added services, analytics depth, and white-label customization with real-world context on what goes wrong when these features are missing.

If you are analyzing custom mobile wallet solutions for the first time or re-platforming from a legacy stack, this guide gives you the evaluation framework you need to make the right call.

Why the Market Demands Custom Mobile Wallet Solutions?

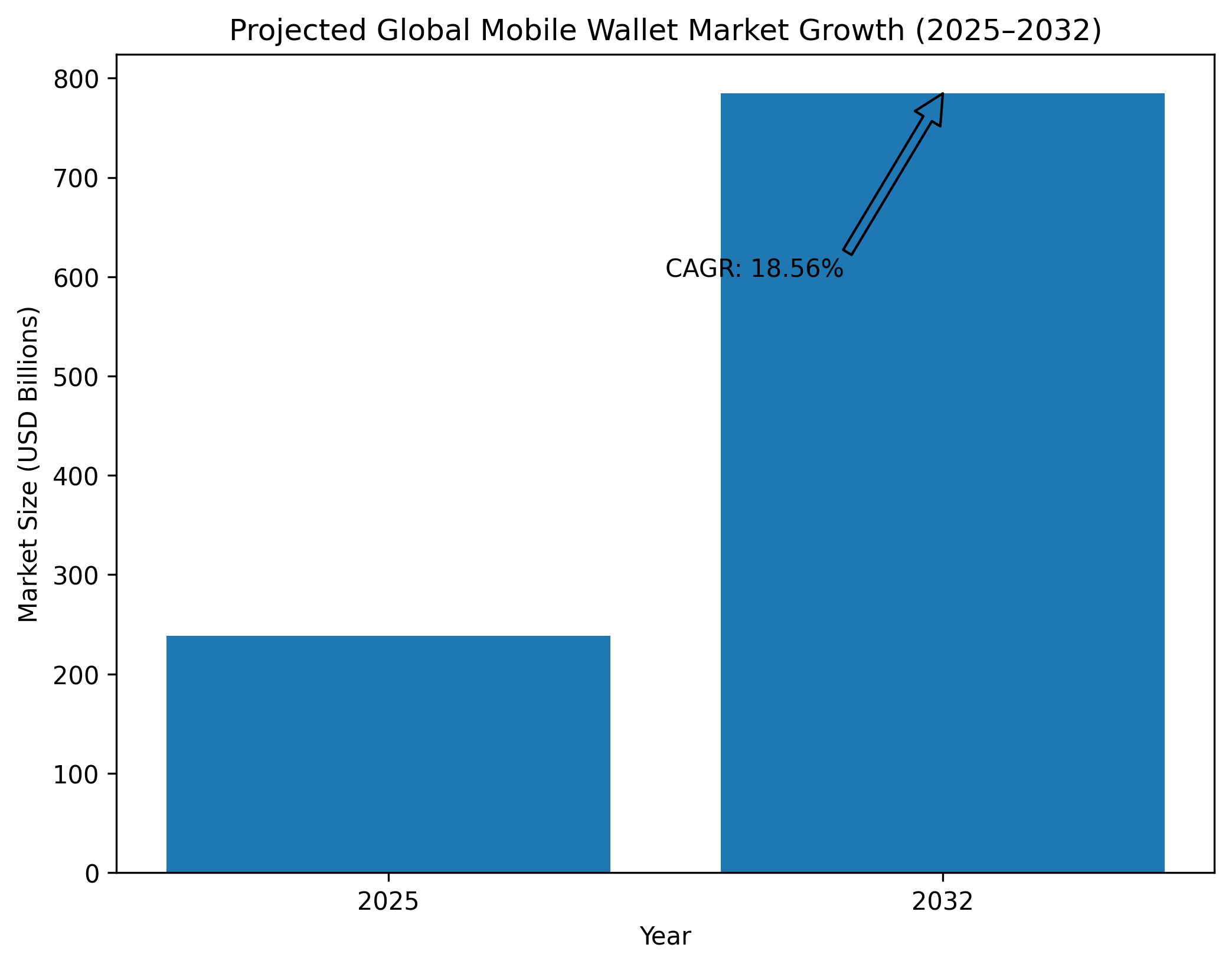

According to Fortune Business Insights, the global mobile wallet market is projected to grow from USD 238.26 billion in 2025 to USD 784.67 billion by 2032, exhibiting a CAGR of 18.56%. Separately, Capital One Shopping’s research found that digital wallet transaction volumes are projected to surpass $17 trillion globally by 2029, growing at an 11.2% compound annual rate from 2024 onward.

Those figures represent real transactions flowing through real infrastructure that your custom mobile wallet solutions must support without flinching. When you factor in the regulatory complexity of digital financial services, the expectations consumers now have around speed and security, and the integration demands of modern commerce ecosystems, it becomes obvious that selecting the wrong vendor can cost far more than a botched implementation. It can cost you customers.

This is exactly the lens through which you should analyze any custom mobile wallet solutions provider, not on the strength of a polished demo, but on the depth of the features underneath it.

Feature 1: Multi-Layered Security Architecture

There is no negotiating on this point. A custom mobile wallet solution that cuts corners on security is not a product; it is a liability. The architecture must address threats at every layer: network, application, data, and device.

The minimum bar you should expect includes PCI-DSS compliance, end-to-end encryption (E2EE), tokenization of stored card credentials, and biometric authentication via fingerprint, facial recognition, and behavioral locking. But the leading custom mobile wallet solutions go further. They incorporate real-time fraud scoring engines powered by machine learning, velocity checks across transaction types, and anomaly detection that flags deviations from a user’s established spending patterns before a transaction is approved, not after it has settled.

When evaluating vendors, ask them specifically how their fraud detection model is trained, how frequently it is updated, and what its false-positive rate is in production environments. A vendor that cannot answer those questions precisely has not solved the problem; they have only shipped a checkbox.

Feature 2: Interoperability and Open API Architecture

A custom mobile wallet solution that cannot talk to the rest of your ecosystem is an island. In practice, this means your chosen platform must offer well-documented, RESTful or GraphQL APIs that allow seamless integration with your core banking system, your CRM, your loyalty engine, your KYC/AML provider, and any third-party payment scheme, whether that is Visa, Mastercard, local instant payment rails, or a proprietary scheme.

This is where many second-tier custom mobile wallet solution providers fall short. They offer pre-built integrations with a narrow set of partners and make connecting to everything outside that set prohibitively expensive. In contrast, the best mobile wallet solution architectures are designed API-first from the ground up, meaning any system that can make an HTTP call can be integrated without heroic engineering effort.

For telecom operators building on top of a mobile device manager software layer, open APIs are even more critical. The custom mobile wallet solutions must be able to push and pull data from the subscriber management system, the charging infrastructure, and the OTA provisioning stack without friction. 6D Technologies’ carrier-grade wallet platform specifically addresses this requirement, having been designed alongside BSS/OSS environments where telco-grade scale and real-time data exchange are not optional features.

Before signing any contract, request a sandbox environment with full API documentation. Run your developers through an integration exercise against your own systems. If the integration takes more than a week for a standard use case, that is a signal about the product’s true openness.

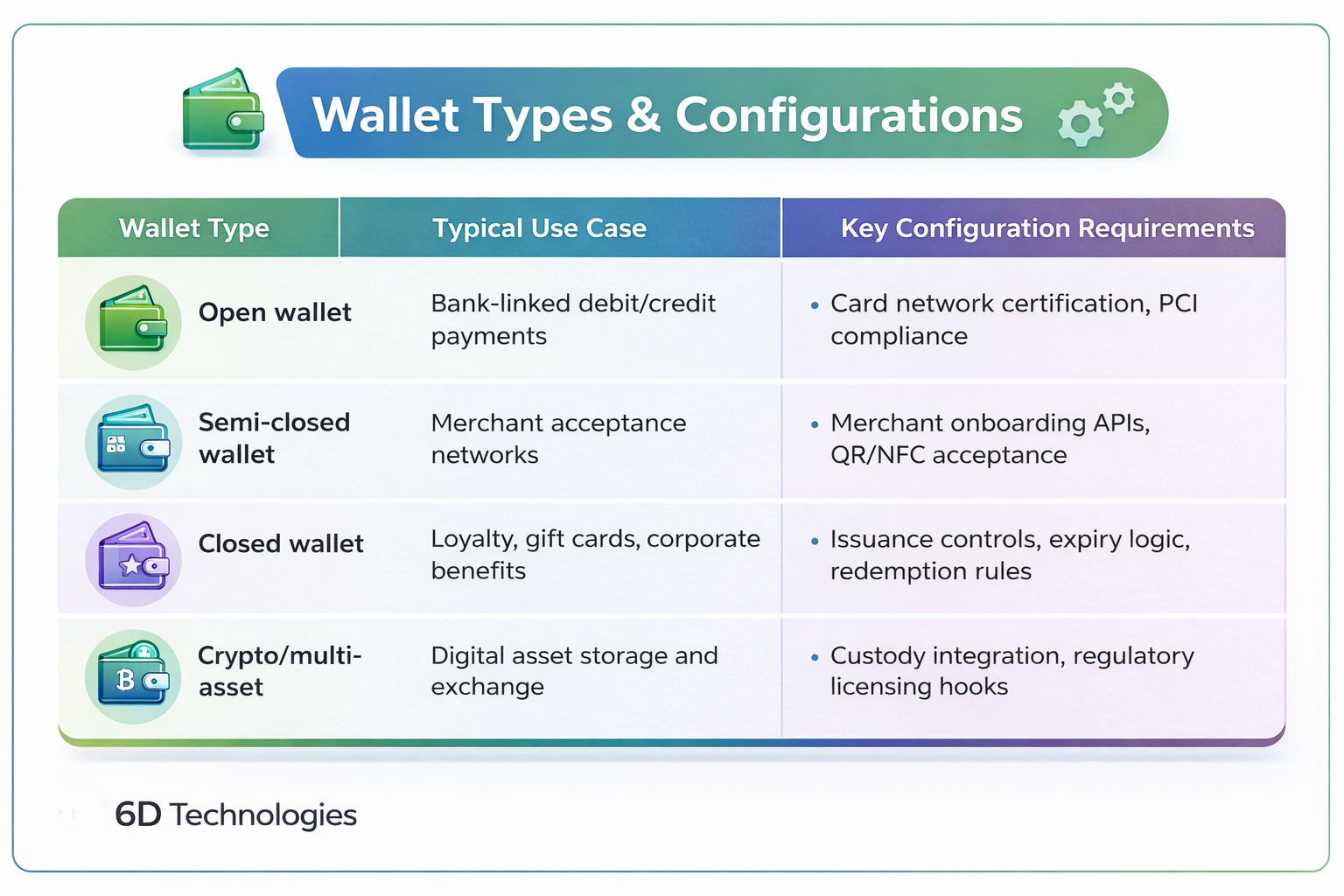

Feature 3: Configurable Wallet Types and Financial Products

Not all wallets serve the same purpose. A consumer P2P wallet for a fintech startup looks nothing like a closed-loop corporate expense wallet for an enterprise, or a semi-closed merchant wallet for a regional retail chain. Your platform must support all of these configurations and the ability to switch between them without rebuilding from scratch.

The best mobile wallet payment solutions support the full taxonomy:

The leading telco companies offer configurable wallet templates across all four categories within their best mobile wallet solution stack, enabling operators to launch new product lines without spinning up entirely new infrastructure. This modularity has been a key differentiator in markets where operators need to serve both banked and underbanked segments.

Feature 4: Real-Time Transaction Processing and Scalability

Consumer patience for payment latency is effectively zero. Any visible delay between tap and confirmation erodes trust. And when trust is once lost in financial services, it’s very difficult to regain. Your mobile ewallet platform must be engineered for real-time processing at scale, with sub-second authorization responses across normal operating conditions and degraded-mode resilience during peak loads or partial outages.

This requires a distributed, cloud-native architecture with horizontal scaling, active data center configurations, and circuit breakers to prevent cascading failures. It also requires rigorous performance benchmarking, not theoretical throughput figures, but documented peak TPS (transactions per second) measured under production-representative load profiles.

Feature 5: Regulatory Compliance and Licensing Support

Digital financial services regulation is not static. The regulatory landscape shifts across jurisdictions; FinCEN rules in the U.S., PSD2 in Europe, RBI guidelines in India, CBN frameworks in Nigeria, and your custom mobile wallet solution must be able to adapt to those changes without requiring a platform re-architecture every time a new directive lands.

This means the compliance engine must be configurable, not hardcoded. KYC tier levels, AML screening rules, transaction limits, cooling-off periods, and reporting obligations must all be adjustable through administrative controls rather than source code changes. The best mobile wallet solution providers embed compliance as a product feature.

Ask every vendor you evaluate for a compliance configuration matrix that maps their platform capabilities to the specific regulatory frameworks in your target markets. If they hand you a generic compliance checklist, push harder. You need jurisdiction-specific evidence, not marketing language.

Feature 6: Merchant and Agent Network Management

A custom mobile wallet solution without a merchant acceptance network is a product in search of a problem. The platform must come with tooling to onboard, manage, and settle with merchants, including both large-format organized retailers and the informal small-merchant segment that represents the majority of transaction volume in many high-growth markets.

This includes QR code generation and management, POS SDK libraries for in-app and hardware-based acceptance, merchant analytics dashboards, dynamic settlement configurations, and agent banking workflows for cash-in/cash-out operations. The underlying mobile device manager software integration that governs device-level controls, particularly for agent point-of-sale devices, should also be native to the platform or available through a clean integration layer.

Our agent banking module is a case in point. Our platform supports hierarchical agent structures, master agents, sub-agents, and retail agents with individual commission configurations, float management, and real-time liquidity monitoring. For operators in markets where physical agent networks still handle a significant share of cash-to-digital conversion, this capability is not a nice-to-have. It is a go-to-market requirement.

Feature 7: Loyalty, Rewards, and Value-Added Services

Payments drive adoption. But loyalty and value-added services drive retention, and retention is where the economics of a mobile ewallet platform actually work out. Users who engage with rewards, cashback, buy-now-pay-later (BNPL) micro-credit, insurance, and savings products churn at dramatically lower rates than users who only transact.

The platform must support a composable services layer that allows operators to attach financial and non-financial services to the custom mobile wallet solutions without having to build each one from scratch. This includes a loyalty engine with configurable earn-and-burn rules, a BNPL credit module with risk-scoring hooks, micro-savings vaults, bill payment aggregation, and remittance corridors.

The best mobile wallet solution architectures treat the wallet as a platform, a surface on which new financial products can be launched iteratively rather than a fixed product with a finite feature set. We explicitly position wallet offering this way, providing operators with the infrastructure to upgrade from a payments utility to a full-stack digital financial services hub over time.

Feature 8: Analytics, Reporting, and Business Intelligence

You cannot optimize what you cannot measure. The platform must provide granular, real-time analytics across every dimension of wallet behavior: transaction volumes, user activation and churn, merchant settlement performance, fraud incident rates, feature adoption, and cohort-level revenue metrics.

This intelligence should be accessible through both a built-in operator dashboard and via data export APIs that connect to your own business intelligence stack. Leading custom mobile wallet solution providers also offer pre-built regulatory reporting templates that automate the generation of central bank compliance reports, a capability that reduces significant operational overhead for any licensed operator.

During vendor evaluation, request access to the standard reporting package and the data export schema. Run a quick exercise: can your data team answer a specific business question? Say, the 30-day retention rate of users who activated a loyalty card within their first week from the available data? If it takes a support ticket and a custom extract, the platform’s analytics maturity is not where it needs to be.

Feature 9: White-Label Customization and Branding Control

Operators building a branded mobile wallet payment solution need deep customization capability, not just the ability to swap a logo and a color palette. The platform must support full UI/UX theming, configurable user journeys, branded onboarding flows, and the ability to launch regional or segment-specific wallet variants under a unified backend.

6D Technologies’ white-label custom mobile wallet solution framework is designed precisely for this use case, allowing telecom operators, banks, and fintechs to deliver a fully branded customer experience without building or maintaining the underlying platform themselves. The operator controls the front end. The platform handles the back end. This clean separation reduces time-to-market for new branded launches from months to weeks.

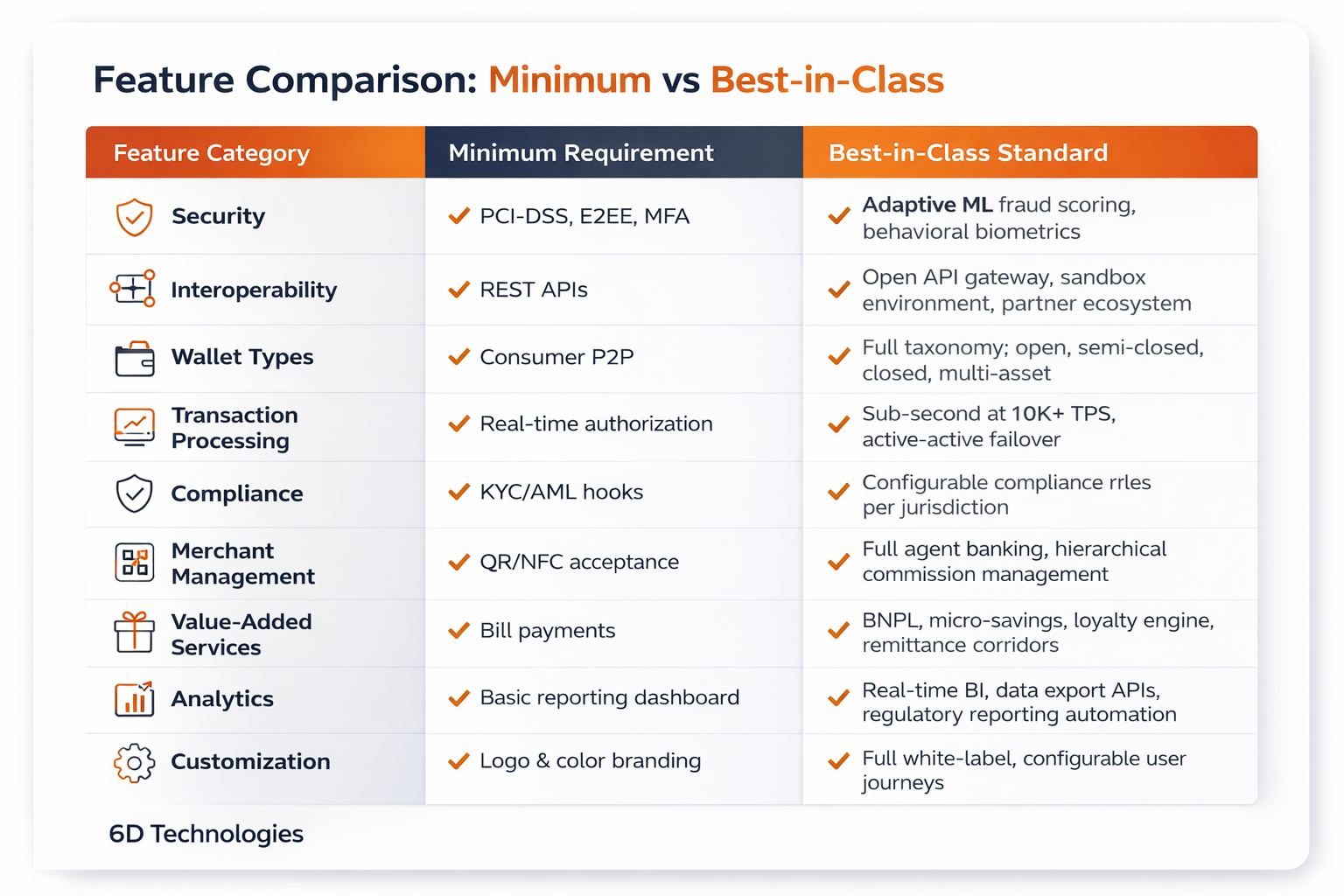

A Feature Checklist: What to Demand from Any Custom Mobile Wallet Solution Provider

Before you finalize your partner evaluation, run every team member through this checklist. No single feature in isolation is sufficient. It is the combination that defines a capable platform.

Real-World Context: What Happens When Features Are Missing

Consider a mid-size telecom operator that launched a mobile wallet in 2022 without a configurable compliance module. When the local central bank updated its tiered KYC thresholds, a routine regulatory adjustment, the operator needed six months and a significant platform engineering investment to implement the change. Six months of operating outside updated guidelines, with associated legal risk and the operational cost of a manual workaround, all because compliance configurability was not treated as a first-class platform requirement at procurement time.

Contrast this with operators who built on platforms designed with regulatory flexibility from the outset. Those operators implemented the same change in under two weeks through an administrative configuration update. The difference is not marginal. In regulated digital financial services, it is the difference between being a compliant operator and being a compliance problem.

This pattern, where feature gaps are invisible at demo time become operational crisis post-launch. Repeats across every category on the checklist above. The cost of evaluating thoroughly is a few extra weeks. The cost of evaluating poorly is measured in years.

Conclusion:

Choosing a custom mobile wallet solution is one of the highest-stakes infrastructure decisions a financial services operator makes. The features covered in this blog are not a wishlist. They are the baseline of what any top-rated custom mobile wallet solution providers must deliver before it earns the right to be in your shortlist.

Here are the key takeaways from everything covered above:

- Security is non-negotiable: Multi-layer authentication, tokenization, E2EE, and real-time fraud detection are table stakes, not differentiators.

- Open APIs determine your ecosystem potential: A closed platform limits your growth. An API-first architecture enables it.

- Configurable compliance is a strategic asset: Hardcoded regulatory logic will cost you dearly every time the rules change.

- Real-time, scalable processing is a product feature: Latency and downtime in payments are not technical issues; they are customer experience failures.

- Merchant and agent tooling drives adoption: Without an acceptance infrastructure, a wallet is just an app.

- Loyalty and value-added services drive retention: The economics of custom mobile wallet solution businesses depend on engagement beyond payments.

- Analytics enable optimization: You need data to grow. Platforms that restrict data access restrict your ability to compete.

- White-label flexibility protects your brand equity: You should own the customer relationship, not your platform vendor.

- Always validate in a sandbox: Claims made in sales presentations are hypotheses. Integration performance is evidence.

The best mobile wallet solution is the one that grows with your ambitions, not the one that forces you to grow around its limitations.

Ready to Build a Custom Mobile Wallet Solution That Does More?

Selecting the right partner is as important as selecting the right features. The market for custom mobile wallet solutions is crowded, but very few vendors combine carrier-grade scalability, regulatory configurability, open API architecture, and deep digital financial services domain expertise under one roof.

6D Technologies is one of the industry’s most trusted providers of custom mobile wallet solutions and mobile ewallet platform infrastructure, with deployments across telecom markets. Its platform is engineered to meet the exact feature requirements detailed in this blog, from adaptive fraud detection and configurable KYC workflows to agent banking management and composable value-added services.

If you are assessing mobile wallet solution providers and want to see how a purpose-built, enterprise-grade platform performs against your specific requirements, feel free to connect with us to discuss your requirements and a detailed walkthrough of a mobile wallet and digital financial services platform.

FAQs

What are the must-have features of a custom mobile wallet solution?

Any enterprise-grade custom mobile wallet solution must deliver multi-layered security (PCI-DSS, E2EE, tokenization), open API architecture, configurable compliance controls, real-time transaction processing, merchant and agent network tooling, loyalty and value-added services, and full white-label customization. A mobile ewallet platform missing any of these will cost you far more to fix post-launch than it would have to evaluate properly upfront.

How do I choose the right custom mobile wallet solution provider?

When evaluating custom mobile wallet solution providers, test before you commit. Request a sandbox environment, run a real integration exercise, ask for jurisdiction-specific compliance documentation, and demand production-verified TPS benchmarks, not theoretical figures. The right mobile wallet payment solution partner should answer all of these without hesitation.

What is the difference between an open, semi-closed, and closed mobile wallet?

An open wallet works anywhere, linked to a bank or card network. A semi-closed wallet works within a defined merchant network without cash withdrawal rights. A closed wallet is restricted to a single brand or platform, like a gift card or corporate benefits wallet. A capable custom mobile wallet solution supports all three configurations under one backend, making it far easier to serve diverse customer segments within your digital financial services portfolio.

How secure are mobile wallet payment solutions?

Security standards vary widely across mobile wallet payment solutions. At minimum, look for PCI-DSS certification, E2EE, tokenization, and MFA, including biometrics. The best mobile wallet solution providers go further, adding ML-based fraud scoring and real-time anomaly detection that flags suspicious activity before a transaction settles. Always ask for a vendor’s documented false-positive fraud rate in production; it reveals more than any security checklist will.